Article by Patrick Evans | Photography by Audrey Merkel | Owl Staff

Earle Anderson, a Psychology major at HCC, was 19 when he moved out of Catonsville to live on his own in Bel Air. That’s when the struggle began.

“I’ve had to work multiple jobs, I’ve had to have more people in my apartment than there are bedrooms, I’ve had to skip meal…,” Anderson says.

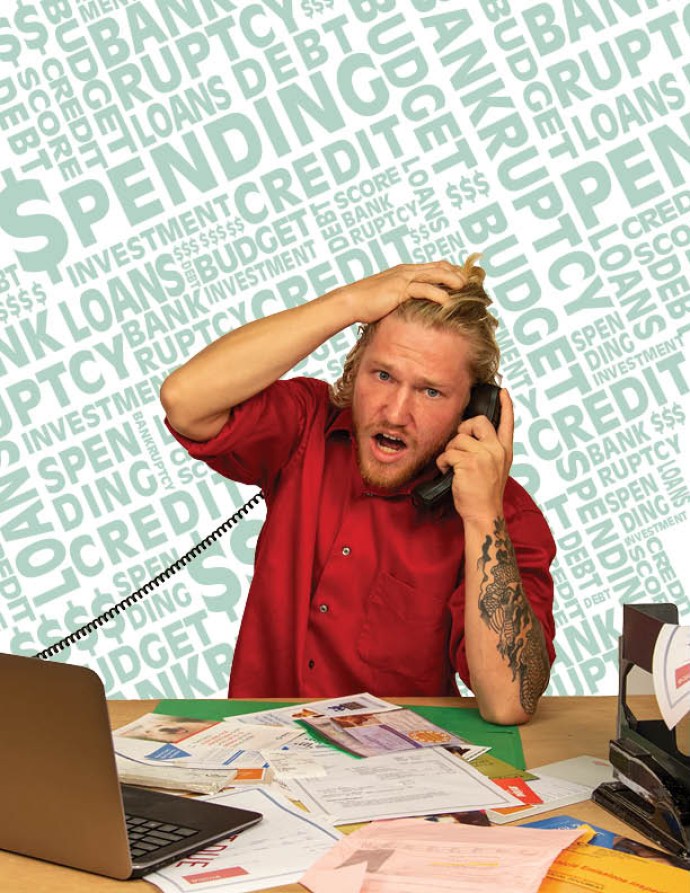

Managing your money can seem almost impossible when you’re starting out. Creating a budget plan is one of the most important things you can do for your finances. However, students like HCC Music major Daniel Woods know this is easier said than done.

Woods says, “By the time I left [school] last fall, I was completely broke. Both of my checking accounts were in the negative. My savings account was empty. My credit card was maxed out. I couldn’t do anything!”

Woods was only able to escape his predicament by paying closer attention to his finances. He continues, “From then on, I was working on keeping track of my finances – every little bit I’m spending, every little bit that’s coming in – then I’d make a monthly log for that.”

Logging where your money is going can be as easy as using a pen and paper, but you may opt to utilize spreadsheet applications like Microsoft Excel. Companies like Quicken and Personal Capital also offer many useful budgeting tools to steer you in the right direction.

Part of knowing where your money goes is keeping track of how much money you spend on non-essential items. In life there are needs and wants; wants are unnecessary purchases. An example of a non-essential buy could be eating out at a restaurant rather than paying less for eating at home.

“Say you want to go out with your friends,” begins Cheyenne Polanco, General Studies major at HCC. “Learn how to say no because you can’t do it. Sometimes you just gotta stay in the house and stack your money up…”

If you’re on a budget, discerning between food options becomes more important. Even though name brand items tend to sell more, the cheaper off-brand alternatives can be just as good. With a little research, you can limit spending on non-essentials.

“Budgeting your money takes a lot of discipline. You need to be able to say ‘no’ to stuff you might really want. You need to constantly remind yourself you are budgeting and set money goals, so you have something to look forward to,” Woods states.

“Managing your money can seem almost impossible when you’re starting out.”

It’s especially important to keep realistic goals when budgeting, and being realistic means setting a reasonable timetable. For example, expecting to pay off an expensive car or a large student loan in a year is unreasonable. Shortterm goals could include making smaller single payments to make progress on larger obligations.

A money-saving practice many adopt is to use cash in lieu of a debit or credit card whenever possible. You can be more cognizant of spending money when a transaction of physical objects is involved. You can see instantly that $20 is missing from your wallet, unlike with a credit or debit card.

However, credit cards are a useful and important tool for students. A credit card can allow you to make payments when you don’t quite have the funds you need yet, and to build credit. Many credit cards even have perks and rewards for using the card responsibly.

Many companies offer benefits to students. The Discover it card offers rewards like 5 % cash back at various places such as gas stations, grocery stores, and restaurants.

Most credit card companies would love to have your business, but it’s important to educate yourself and find the best possible deal for your situation.

“Read all the fine print, understand what the repayment terms are, and what the interest rate is. A lot of credit cards will give you a ‘teaser rate’ then convert at a certain point in time,” states Denise Kratz, Vice President and Quality Assurance Operational Manager at Sandy Spring Bank in Maryland.

You should consistently pay your credit card bill each month. Leaving these bills unpaid can lead you to develop a bad credit score, which will lessen your chances to qualify for a loan in the future.

One of the biggest difficulties Anderson faced after striking out on his own in Bel Air was keeping his credit card under control.

“I did not read all of the fine print nor bothered to look into how a credit card actually worked. I assumed that if I didn’t pay [the bills] at the end of the month, they (the credit card company) would call me or send me something in the mail…but they don’t,” Anderson says.

He continues, “I became so reliant on my credit card that the original problem snowballed into this much bigger issue that I must now address.”

The importance of your credit score can be difficult to understand at first. Many people only become aware of their poor understanding of credit when it becomes a problem.

Anderson says, “I thought I [knew]. I knew it was a number, and I knew [the score] measured something about me … if it was good, I could get a house. If it was bad, my life was ruined.”

Losing track of credit can happen to anyone, even a financially stable adult. In recent years, a professor at HCC hasbeen recovering from a tough time with credit.

“When I was married, I was very hands-off with the finances … It wasn’t until we were separated that I started being the one to really manage the finances and manage the budget,” the professor says.

Not paying credit card bills on time isn’t the only thing that hurts your credit score. Missing payments on student loans is also detrimental. Your credit score can drop rapidly when left unchecked.

“Many people only become aware of their poor understanding of credit when it becomes a problem.”

The professor continues, “Mounting legal bills and missed student loan and credit card payments brought down my score by 200 points. I ended up in a situation where I was in danger of losing my house. I was still considered a risk to the bank because my credit score was not good.”

While all may seem lost if your credit score plummets, the situation is still salvageable. It may take a while to get back to a good score, but it isn’t impossible.

“If I had not worked so hard to turn my credit score around, I might have lost my house even though I had the ability to make the mortgage payment,” says the professor.

HCC Computer Aided Design and Drafting major Michael Rayner, who now sports a credit score of 840, started improving his score when he was denied something he wanted based on his credit.

“It was from that point on I decided to educate myself so I would never experience that disappointment again,” he says.

Rayner advises other students to “find the best way to establish credit, which comes in many forms, such as a credit card, car loan, or personal loan. Starting small and taking manageable steps can help the process come easier … Eventually by making on-time payments and never exceeding 30% usage of available credit, your overall credit limit and score will increase.”

Like managing credit, managing debt is paramount to financial success. The best way to manage debt is to avoid taking out loans, but sometimes, loans are unavoidable. Students who have to pay their own way through college frequently end up in significant student loan debt.

This debt can add up quickly. According to Debt.org, the average outstanding student loan debt was over $37,000 in 2017.

Student loan debt doesn’t go away until you pay it off. It’s not dischargeable in bankruptcy; this fact places a heavy burden on those who have had to borrow funds for school. If student loan payments are not made on time, there will be late fees and other penalties.

Loans can also have a long-lasting ripple effect. If you are already deep in debt, you may not be able to qualify for a credit card.

“As soon as the [credit] card company looks at [your loan] …they may not give you a credit card … It may hinder your next borrowing attempt,” states Chuck Jacobs, former President of Harford Bank.

While student loans may seem scary, you don’t have to face them alone. Colleges offer a variety of resources to keep you informed and updated on your school finances.

As Jacobs says, “Most colleges of any size will walk you through student loans.”

If possible, take out only one loan at a time. Hopefully, you won’t need a house or car right away. It’s important to know where the loan is coming from. Sometimes it’s easy to get talked into a dangerous predatory loan.

Usually, predatory loans target those who have bad credit and need a loan. These loans often have unreasonably high interest rates, only benefiting the lender in the long run.

Luckily, most states have regulations that help prevent predatory lending. Despite these protections, you should always be wary.

“If it seems too good to be true, it probably is. Always use a reputable company,” states Jacobs.

A highly regarded lender, like a commercial bank, will usually be federally insured and federally regulated. Local reputable banks include Aberdeen Proving Ground Federal Credit Union and Harford Bank.

Before you consider taking out a loan, you should have money already saved. While putting funds into a savings account is beneficial, they can grow further if they’re invested. Investing, rather than simply saving, allows your money to compound at a higher rate.

Ted Kelly, Financial Advisor at Edward Jones Financial, states, “We find that if it is just in a savings account over a long period of time, it’s not going to compound enough to keep up with inflation.”

Investing in the stock market has become more popular among students with the advent of streamlined investment applications like Robinhood and Acorns. However, it’s important to remember that stocks can be high-risk, especially if you choose to make short-term investments in volatile companies.

Financial experts who study the stock market at firms like The Motley Fool, Investopedia, and even The Wall Street Journal can offer valuable insight and advice as to potential investments. However, the stock market is unpredictable by nature.

Starting your own life on the right financial foot will save you time and stress. You can avoid a wealth of unnecessary hardship by keeping track of your money and following advice from the experts.

HCC student Michael Rayner says, “Through this discipline my wife and I were able to purchase our dream house, drive the vehicles we desire and provide a stable financial future for ourselves.”